Home sellers should consider a Short Sale when the value of their home is LESS than the amount of their outstanding loans. For example, if your home is worth $250,000 but you have a loan of $260,000 then a short sale is a consideration.

First we must figure out the true value of your property. We can provide you with a market analysis and give you a good idea of what your home might sell for If the market is moving down keep in mind that your homes value may be moving down as well and estimated valuations may be valid for only a short time.

- We’ll also need to calculate your estimated closing costs. Items such as a title report, escrow, appraisal, attorney fees, agent commissions, unpaid property taxes etc.

- We’ll need to know how much you owe on your property. Include all loans on the property in your calculation.

- Calculate your equity. Normally the value of your home is more than the total of the loans and closing costs. If your closing cost estimate plus your loan amounts are higher than the value of your property then a short sale is a possibility.

- We’ll need to contact your lender and explain your situation. Be sure you talk to someone who has the authority to make the required decisions. Usually lenders have a loss mitigation department we you can contact. Lenders are under no obligation to accept a short sale but many times it is in their best interests to do so.

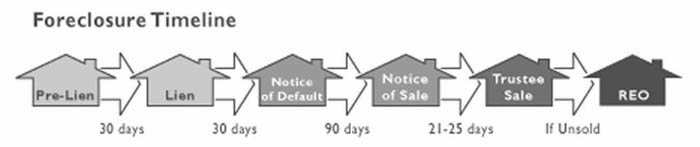

- Some lenders will not consider a short sale until you have missed a payment or two. Some will not accept short sales at all. We’ll need to know where your lender stands with regard to short sales so we’ll need to contact them as soon as possible.

- Consider your tax obligations! Do not underestimate this! Many times there can be a substantial tax obligation after a short sale has occurred. Be sure to talk with an accountant or tax attorney to figure out how much money you may owe the IRS if you proceed with a short sale. The link above to the IRS site explaining, who can have the debt forgiven has a wealth of information on this.

- Find a buyer and sell your property. The lender will still have to approve the buyer’s offer but once they do you can sell your property.

- They go through their internal process of BPO and appraisal. It differs from lender to lender. The reason is the same at each one. They want to determine the loss on the mortgage. They will also calculate what the additional loss will be if they don’t cooperate with a short sale.

- When they realize the short sale will potentially save them thousands of dollars, usually after the appraisal. They move on to approving the short sale and producing a document authorizing the closing of the escrow.

Leave a Reply

Want to join the discussion?Feel free to contribute!